As China has become a major global economy and grows more assertive on the global stage, the country has discovered the power of anti-trust legislation. While created on three common pillars of fighting anti-competitive agreements between companies, the abuse of a dominant position, and mergers that may eliminate or restrict competition, the implementation is increasingly different. There have been hundreds of cases where Chinese authorities have looked at mergers between Chinese companies, and not one has been objectionable to the authorities. But if it doesn’t matter that two separate companies are owned by the state or merged, how can a merger between state-owned businesses be anti-competitive?

In a state capitalist system, as we have now, Communist Party groups are part of every company, including private domestic or international joint-ventures and all foreign investment is in the shape of a joint-venture with a Chinese partner with three or more employees. While they have long-established formal power in state owned enterprises (SOE), for joint ventures there is increasing pressure to allow party groups to approve all critical matters before they are presented to the board based on the 2017 Communist Party Directive entitled “Notice about firmly promoting writing SOE party building work into company articles of association.” Following this logic, reviews of intra-Chinese mergers have always been approved.

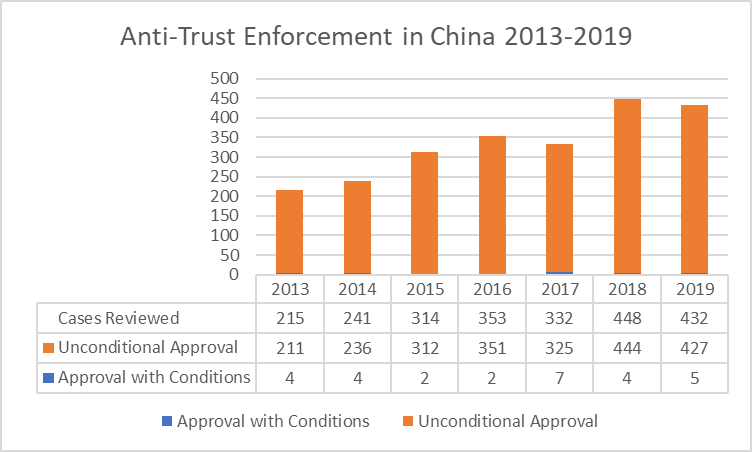

Mergers in the last decade

As you can see from the chart above, there are no outright merger rejections and only a small number of approvals with conditions. Interestingly, the only mergers that have come under scrutiny are mergers without Chinese involvement. Due to the extraterritorial nature of Chinese anti-trust law, even mergers of companies outside China fall under its purview when it involves companies with a substantial amount of business in China. For example, in 2019, the five cases that were approved with conditions were KLA Tencor (US)/ Orbotech (Israel), Cargotec (Finland)/ TTS (Norway), II-VI incorporated (US)/Finisar (US), Zhejiang Huayuan Biotechnology (PR China)/Royal DSM (Dutch), and Nevelis (US)/Aleris (US). In addition, there are cases like Qualcomm (US) / NXP (Dutch), where instead of denying the application, Chinese anti-trust authorities just ran out the time. After two years of waiting for the acquisition of NXP by Qualcomm to be permitted, the companies reached the end of the contractual merger period and were forced to give up. This de facto denial was never recorded as a denial, as the Chinese anti-trust authorities simply did not rule. Due to the small size of China’s anti-trust authority, the country has plausible deniability when it delays ruling on a merger. At face value, China’s perfect record of only approving mergers remains intact, when in reality the merger was forcibly abandoned.

What’s really at stake

Cases such as those mentioned above create the appearance that Chinese anti-trust concerns are not directed at protecting Chinese consumers but protecting Chinese industrial policy. The approval with conditions of the Marubeni (Japan) acquisition of Gavilon (US) and Glencore (Swiss) of Xstrata (Swiss/UK) demonstrates that China’s industrial policy leads anti-trust merger enforcement. In both cases, China was concerned about the supply of vital commodities, copper and grain respectively, and the merger was approved only after significant divestitures that alleviated these concerns.

With this in mind, the acquisition of ARM Technologies (UK) from Softbank (Japan) by Nvidia from the US will be another interesting case. Most casual observers would conclude that Chinese anti-trust authorities would not be involved. Au contraire, mon ami! Almost all smartphone central processors are using ARM instruction sets, and Chinese companies have built their AI and neural processing technology on them. Huawei even went a step further and built its Ascend AI and Kunpeng general purpose processor programs entirely on ARM. The increasing reliance is due both to technical and to political reasons.

President Trump’s moves to use American intellectual property in trade battles with China, as well as restricting their use in military and dual-use applications, has complicated the lives of Chinese high-tech companies and it is likely to continue during President Biden’s administration. As a reaction, China has accelerated its Made in China 2025 project focused on reducing its dependency on foreign technology and products and shifting to non-American suppliers. If the Nvidia acquisition of ARM goes through, another key technology will be more closely under the control of US authorities, giving them another potential tool to assert pressure on China. It would also give Nvidia a significant boost in the AI competitive race that China considers one of its highest priorities. Nividia is a leader in network-based AI and ARM a leader in device-based, also known as edge AI. Combining the two companies makes them a much more formidable competitor, allowing to cross pollinate network AI with edge AI technology and vice-versa. Both companies have substantial business in China and hence fall under Chinese anti-trust laws and are subject to review.

Considering China’s track record, it is almost inevitably going to either block or just refuse to approve the Nvidia/ARM transaction to protect its domestic industry from further US sanctions and restrictions and to prevent a stronger competitor in the AI marketplace. It is more likely that China will simply run out the clock on the merger, while a more aggressive and higher profile move would be an outright denial of the merger. This would send a much stronger signal to the United States than passive aggressive non-approval and would be a harbinger of a more adversarial phase in the relationship between the two countries.