The wireless industry has a Walmart problem. Not because Walmart is hostile to carriers or OEMs, it’s quite the opposite. The problem is that Walmart has quietly become the single most important physical destination for wireless shopping in the United States, and no carrier directly controls what happens inside it. Many Walmart wireless departments operate through third-party firms like Premium Retail Services, OSL, and T-ROC, whose representatives work the floor under Walmart contracts rather than any carrier’s payroll. Carriers have contractual pathways into this model, but none have deployed them at the scale the foot traffic data now warrants.

According to new data from the Recon Analytics US Consumer Device Purchase Journey report series, which tracks more than 100,000 US respondents over five consecutive quarters from Q4 2024 through Q4 2025, Walmart Supercenter accounted for 17.4 percent of wireless store visits in Q2 2025. T-Mobile, the closest competitor, checked in at 16.1 percent. AT&T trailed at 12.8 percent. Verizon at 12.5 percent.

Let that sink in for a moment. A big-box retailer best known for groceries and $6 t-shirts is pulling more wireless foot traffic than the country’s most-subscribed carrier. And the people walking through those doors look nothing like the customers carriers typically design their promotions around.

The Prepaid Goldmine Nobody Owns

Half of Walmart’s wireless visitors, 50.8 percent, earn under $50,000 annually. That’s 4.7 points above T-Mobile stores, whose under-$25K visitor concentration already exceeds that of AT&T or Verizon. At the other big-box formats, Costco skews almost precisely the opposite direction: 19.6 percent of Costco wireless visitors come from the $100K–$149K bracket. These two stores are not serving the same customer, and treating big-box retail as a monolithic channel is a strategic error.

What makes Walmart particularly consequential is the prepaid concentration. Straight Talk and Tracfone together account for 9.9 percent of Walmart wireless visitors, three to five times the rate recorded at every other major retail location in the dataset. Factor in Cricket and Metro by T-Mobile, and nearly one in five Walmart wireless visitors currently carry a prepaid or MVNO plan. These are the exact consumers every major carrier wants to convert from prepaid to postpaid. They are clustered at a single, high-traffic physical location. And no carrier owns that location.

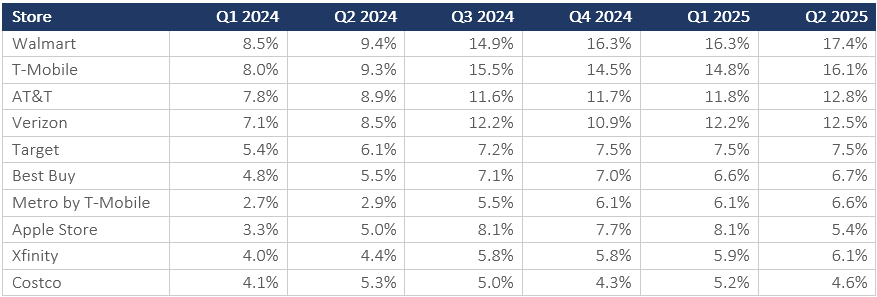

The table below shows how dramatically Walmart’s visitation share grew over six quarters, moving from statistical parity with T-Mobile in early 2024 to a clear lead by mid-2025.

Table 1: Store Visitation Rates by Quarter (% of Respondents), Q1 2024 – Q2 2025.

Source: Recon Analytics US Consumer Telecom Distribution Module Survey. Sample sizes range from 4,588 to 14,392.

The practical implication is direct: any carrier promotion designed to drive postpaid conversion needs to be built around households earning under $50,000 and being present in Walmart’s wireless section. However, in this income segment, the traditional credit-score-based approach for postpaid needs to be modified to mitigate credit-related risks. The research also identifies the offer threshold that motivates potential switchers. A free iPhone with trade-in activates 23 percent of potential switchers, nearly 10 percentage points above the equivalent Android offers. That sets a specific, high-cost floor for conversion economics that carriers cannot negotiate away.

Word of Mouth Is Still Running the Show

Before consumers walk into any store, they research. And there the industry’s assumptions break down in a different direction. Ask a carrier strategist where device research happens, and the answer usually involves something digital. The Recon Analytics data is more specific: friends and family recommendations are the top research sources for every brand, every month, across the full May through December 2025 tracking period. Not online reviews. Not manufacturers’ websites. Not AI. Word of mouth runs at 9.5–13.5 percent across all brand tiers, and it costs manufacturers precisely nothing to reach, because it operates entirely within their existing user base.

The seasonal patterns in the data are as instructive as the absolute levels. Apple’s word-of-mouth rate peaks in July, tracking the iPhone launch cycle almost perfectly. Motorola does the opposite; it peaks in December at 13.5 percent, the highest single-month reading among brands. When a brand’s strongest advocacy moment is gift season rather than device launch season, its buyer base skews toward casual acquirers rather than enthusiast adopters. That distinction matters for how a brand should allocate marketing expenses and which retail channels to prioritize.

The implication for brand equity is uncomfortable for Samsung, Google, and Motorola. Apple’s 71 percent installed-base penetration among 18-to-29-year-olds isn’t just a market-share statistic; it’s a word-of-mouth engine compounding with every person who joins the iOS ecosystem. Every satisfaction point (cNPS) Samsung, Google, or Motorola fails to recover is another recommendation that doesn’t get made. Brand satisfaction scores, often treated as a customer-retention metric, are the wireless industry’s most cost-effective marketing channel. Brands that let satisfaction erode are not just losing renewals, they’re defunding their own referral network.

AI Research Is Neither a Premium Behavior Nor a Young Person’s Game

The AI research channel is real, growing, and demographically inconvenient for anyone who assumed it was a luxury behavior.

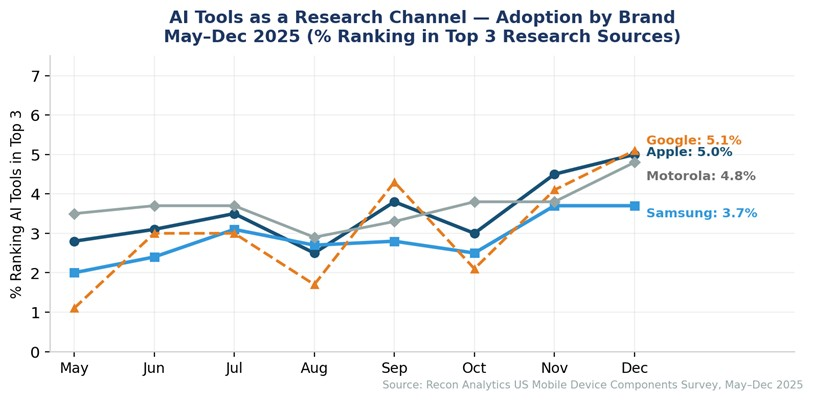

Among Apple buyers, usage of AI tools for device research climbed from 2.8 percent in May 2025 to 5.0 percent in December, a nearly 79 percent increase in eight months. Samsung’s AI research adoption also rose meaningfully, from 2.0 percent to 3.7 percent, while Motorola started the period at 3.5 percent, already above Samsung’s level throughout, and finished at 4.8 percent. That baseline anomaly is analytically significant. Motorola serves a demonstrably lower-income buyer base, yet its adoption of AI research led Samsung from the very first month. The data points to a specific use case: value-segment buyers using AI to navigate spec-to-price comparisons across a crowded $200–$400 Android mid-range market. That is a fundamentally different task from the premium ecosystem research OEM marketing teams typically assume AI serves.

Google’s trajectory requires a structural explanation, not a behavioral one. The apparent climb from 1.1 percent in May to 5.1 percent in December is real in aggregate, but it reflects two distinct product cycles layered atop one another. The June and July readings near 3.0 percent coincide with peak carrier promotional activity for the Pixel 9a. The August collapse to 1.7 percent reflects a research-intensity trough as that promotional window closed — visible simultaneously across friends-and-family, online reviews, and retail visits, not just AI. The December rebound to 5.1 percent is driven by Pixel 10 buyers entering the sample: those buyers use AI research tools at 8 to 11 percent, roughly four times the rate of Pixel 9a or legacy Pixel buyers. As Pixel 10 respondents grew from under 1 percent of the Google sample in August to 10 percent in December, they mechanically lifted the aggregate. Product-cycle awareness matters when reading these trends. A methodological note: Google’s monthly AI tool readings range from 6 to 51 respondents, which means individual monthly readings have wide confidence intervals, and the month-to-month pattern should be read as directional rather than precise.

Figure 1: AI Tools as a Research Channel — Adoption by Brand Tier, May–Dec 2025

The Research Phase Is Where Brands Are Won and Lost

The US Consumer Device Purchase Journey – Part 3 Report findings from Recon Analytics establish the precise mechanisms by which brands enter or exit consumer consideration sets before anyone walks into a store or opens a carrier website. And the picture that emerges is uncomfortable for anyone who has assumed the hard work of brand building happens in the channel.

The research phase is not a passive information-gathering exercise. It is where the consideration set forms and hardens. Consumers who rely primarily on friends and family, the plurality across every brand, are not conducting open-minded evaluations. They are asking people whom they trust whether to do what those people already did. For Apple, with 71 percent penetration among 18- to 29-year-olds, that dynamic creates an almost self-reinforcing competitive moat. Every iOS user is a potential advocate. Every cNPS point the brand sustains above its competitors is compounded through millions of peer conversations that no advertising budget can replicate or intercept.

For Android brands, the arithmetic runs the other way. Google’s word-of-mouth peaked in July at 13.9 percent, then collapsed to 5.7 percent in August, a swing of 8.2 points in a single month, consistent with the opening and closing of the Pixel 9a promotional window, though Google’s monthly sample sizes make single-month readings directional rather than precise. That kind of volatility, where it holds across larger samples, reveals a brand whose advocacy is promotional rather than organic. When the carrier offerings stop, the conversations stop. Samsung shows more structural stability in its word-of-mouth readings, but Apple’s dominant penetration among younger buyers, 71 percent among 18-to-29-year-olds per our previous report (US Consumer Device Purchase Journey – Part 1: Market Landscape, Brand Performance & Consumer Satisfaction – Digital Product Reports), suggests its advocacy engine is structurally deeper, compounding through a cohort that recommends devices to peers at the highest rate of any age group. The AI channel adds a new layer of complexity to this picture. Manufacturer websites are beginning to compete with AI-generated product comparisons for the consumer’s attention during the research phase. The brands that lose this competition are not losing a marginal channel. They are losing the moment when a consumer’s consideration set is still open. Amazon’s role as a neutral research environment, drawing 1.1 to 1.7 percent of cross-brand web traffic regardless of which device a consumer ultimately buys, illustrates the same principle: the early research phase is brand-agnostic terrain that favors whoever has the clearest, most accurate, and most findable product information.

The window is closing. Adoption curves tracked through December 2025 confirm that brands lacking structured, AI-indexed product data are already losing specification comparisons at the discovery stage — before a consumer ever sets foot in a store. This is not a risk to monitor in the future. It is a present one to act on.

—

Note: Data in this article is drawn from the Recon Analytics US Consumer Device Purchase Journey: Part 3, Pre-Purchase Research and Distribution Channel Dynamics. The series covers Q4 2024 through Q4 2025 using the Recon Analytics US Mobile Device Components Survey (n = 104,408 respondents across five quarters). If you are interested in the report, you can find it here: US Consumer Device Purchase Journey – Part 3: Pre-Purchase Research and Distribution Channel Dynamics