RECON ANALYTICS ACQUIRES ATOM INSIGHTS, EXPANDING GLOBAL DEVICE INTELLIGENCE

Boston, MA and Montreal, Canada — March 16, 2026 — Recon Analytics has acquired Atom Insights, a device market intelligence firm with operations in Canada and India. Terms were not disclosed.

Hanish Bhatia, Founder of Atom Insights, joins Recon Analytics as Vice President of Device Intelligence. Bhatia previously served as Associate Director at Counterpoint Research, where he covered global smartphone and device markets for seven years. All employees of Recon Analytics Canada, Recon’s U.S.-based device intelligence group, and its India operations will report to Bhatia.

The acquisition integrates Atom Insights’ global device shipment, sell-through, and component-level intelligence into Recon’s customer research platform, creating the industry’s first end-to-end intelligence service from silicon to subscriber sentiment. Atom Insights tracks device sell-through at the model level across 40-plus countries, covering 400-plus device OEMs and 25-plus semiconductor vendors across smartphones, tablets, wearables and PCs.

“We have spent four years building the customer insights infrastructure that the U.S. telecommunications industry runs on. We built this platform deliberately, like a puzzle, with a connector piece already designed for exactly this moment. We can measure what subscribers experience across 22 dimensions of satisfaction matched to their specific handset hardware, and we know what is inside those devices. What we needed was someone who could tell us how many of them shipped, through which channels, and across which markets. Atom Insights and Hanish Bhatia are the piece we built the that connector for,” said Roger Entner, Analyst and Founder of Recon Analytics.

“Recon is the only firm that can show how a specific handset performs on customer satisfaction matched to real hardware IDs, and tell clients what to do about it,” said Bhatia. “Combining that with Atom Insights’ supply-side data creates a device analytics capability that does not exist anywhere else.”

“Atom Insights lets us answer which device configurations drive satisfaction, which component choices create churn risk, and how OEM decisions ripple through carrier economics,” said Brett Clark, Analyst and COO of Recon Analytics.

Atom Insights’ device intelligence integrates alongside Recon’s Pulse service, on which the largest U.S. telecommunications companies rely for competitive decision-making. Pulse fields more than 15,000 U.S. telecom consumers and up to 1,200 telecom businesses weekly in English and Spanish. Beyond telecom, Pulse reaches 6,000 consumer and business AI respondents, the largest AI customer insights service in the world, and up to 6,000 airline travelers weekly.

Atom Insights’ data will also be available across all three tiers of Recon’s AI platform: Ghost Lab for outside-the-firewall analytics across Recon’s insights and 150-plus third-party databases including speed test data, spectrum data as well as government databases; Recon Enclave deployed inside the client’s firewall; and the Reconnaissance Platform, Recon’s autonomous intelligence system for scenario simulation and decision-ready recommendations.

“The analytical frameworks we have built over four years transfer across industries and geographies,” said Entner. “The device value chain is the natural next frontier, and we intend to keep building.”

About Recon Analytics

Recon Analytics is the largest telecom operator-centric market research provider in the United States, with active verticals spanning AI consumer behavior and commercial aviation. The firm’s dataset includes almost a million device-matched respondents and a historical repository of 2 million-plus total respondents. Our Pulse service delivers near real-time customer insights on a weekly basis answering the specific questions our clients are looking for. Recon delivers intelligence through a three-tier AI architecture: Ghost Lab, Recon Enclave, and the Reconnaissance Platform. www.reconanalytics.com

About Atom Insights

Atom Insights provides model-level device sell-through, shipment tracking, semiconductor market analysis across 40-plus countries and 400-plus OEMs. www.atom-insights.com

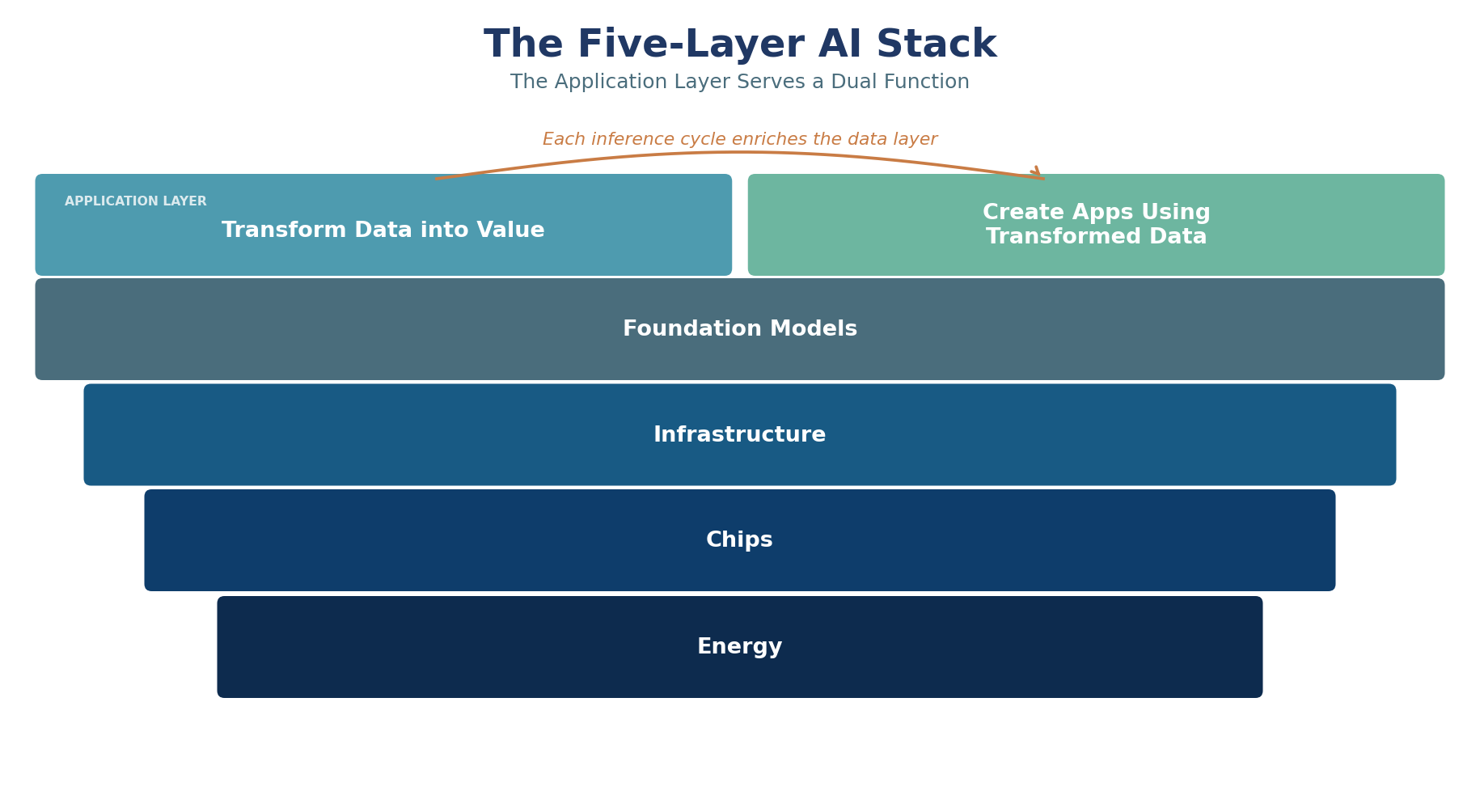

The transformer architecture changed how AI processes information. Now AI is changing how data is processed. Every inference call is an act of data transformation: unstructured input goes in, structured and actionable output comes out.

Jensen Huang framed the AI buildout as a five-layer stack at Davos in January 2026: energy, chips, infrastructure, foundation models, and applications. Each layer serves the one above it. Hundreds of billions invested, trillions still required. https://blogs.nvidia.com/blog/ai-5-layer-cake/

The question is whether value creation at the application layer justifies the capital deployed beneath it. Our reading is that the application layer serves a dual function. It transforms data into value and creates applications that use transformed data.

The tools themselves accelerate this cycle. AI loads information into AI-accessible repositories, builds data dictionaries that facilitate contextual understanding, and creates metadata that speeds retrieval while reducing context consumption. Databases become regeneratively improved resources. Each query refines the schema. Each insight tightens the data dictionary. Each workflow creates reusable context. The database becomes a collaborator, not a repository.

Our survey of 212,382 U.S. respondents between March 2025 and March 2026 tracks where this transformation is working and where it is stalling.

The Integration Gap

Among the 48,330 work users in our survey, the number one feature that would motivate an upgrade from free to paid AI is integration with apps, cited by 22.7%. Improved generative quality comes second at 19.2%.

The satisfaction data tells the same story. Integration satisfaction among work users scores an NPS of negative 10.1, the lowest of any dimension we measure for this group. Overall satisfaction scores positive 9.1. Productivity satisfaction scores positive 5.9. Work users find AI productive. They do not find it connected.

AI is solving its own integration problem. The early phase required users to carry data between tools manually. The current trajectory is direct connectivity: connectors, APIs, and open standards like Model Context Protocol are giving AI live access to databases, CRMs, email, calendars, and document repositories. AI enriches the data it touches, builds context from usage patterns, and makes each subsequent query against that data more productive. The integration gap is closing because AI is the mechanism that closes it.

Huang’s five-layer stack is the right framework. Our data adds a dimension to it: the application layer is not just consuming infrastructure, it is improving the data that feeds back into the stack. The integration gap measures how much of that feedback loop remains to be connected. As connectivity improves, the return on every layer beneath it compounds.

The Transformation Premium

Users start with retrieval: web search, writing assistance, topical research. These require no user data. As users build fluency, they move toward transformation: data analysis, software coding, workflow automation. These require enterprise data. The economic difference is substantial.

Users who employ at least one transformation use case convert to paid subscriptions at 31.6%. Retrieval-only users convert at 13.3%. That is a 2.4x differential across 113,121 respondents. Software coding users convert at 40.2%. Automation users at 37.0%. Data analysis at 31.3%. The baseline for web search is 16.6%. Every metric moves in the same direction: users who connect their data to AI pay for it.

Among workers using AI, 64.9% save three or more hours per week. The value is not the hours saved. It is what those hours produce. Workers with paid AI tools perform analysis they could not previously perform, on data they could not previously access, at speeds that make the work economically viable for the first time. This is expanded output, not cost savings.

Implications for the Stack

The return on AI infrastructure investment is not measured in model benchmarks. It is measured in the volume and value of data transformations the economy can now perform. Cost savings create one-time value capture. Expanded output creates recurring value, drives additional inference demand, and justifies additional infrastructure investment. The flywheel is real. But it runs on data connectivity, not model capability.

The 56.3% of active users who increased their AI usage in the prior three months are climbing the transformation curve. The 19.7% of work users who say they would never pay represent users who have not yet encountered a use case that touches their own data, or whose employers restrict AI integration with enterprise systems. Both conditions are temporary.

The embedded AI thesis assumed that placing AI inside productivity tools would solve the integration problem. Our data from the Recon Analytics User Illusion report suggests otherwise: Microsoft Copilot lost 7.3 percentage points of paid subscriber share in seven months despite being embedded in the most widely deployed productivity suite in the world. Embedding AI inside one application does not help when the work crosses applications. The integration gap is not between the user and AI. It is between the data sources AI needs to access.

Standards like Model Context Protocol address this directly. Rather than embedding AI inside every application, MCP allows AI to reach across applications from a single interface, connecting to databases, CRMs, email, calendars, and document repositories simultaneously. The platforms that build trusted connectors to enterprise data will capture the transformation premium. The platforms that confine AI to a single application will continue to lose share to those that do not.

The regenerative data layer is what makes the infrastructure investment compound. Unlike previous technology cycles where hardware depreciated and software required constant replacement, AI-enriched data environments improve with use. The data dictionary grows. The context layer deepens. The retrieval cost per query declines. Every dollar of infrastructure investment seeds a data asset that becomes more valuable over time.

The trillion-dollar question behind Huang’s stack is whether the applications at the top justify the infrastructure at the bottom. Our data says they do, but only when AI can reach the data. The 22.7% of work users asking for integration are telling the industry what comes next. The capex has been deployed. The models work. The data is there. The returns now depend on connecting them.

Methodology: Based on the Recon Analytics U.S. AI Survey, 212,382 business and consumer respondents surveyed between March 14, 2025 and March 6, 2026. Upgrade trigger analysis based on 48,330 work users and 57,863 home-only users. Paid conversion analysis based on 113,121 respondents with free or paid status recorded. Productivity NPS uses standard NPS methodology (promoters minus detractors on a 0–10 scale). Integration NPS based on 43,718 work users with satisfaction scores. Willingness to pay based on 21,915 work users who named a price. Note: The AI100045 use case battery was expanded in Q3 2025, creating a discontinuity in adoption rates for that question series; use case adoption rates cited in this paper are drawn from the AI100020 series, which remained consistent across the full survey period. All percentages unweighted. Recon Analytics is an independent research firm. This analysis was not commissioned or funded by any AI platform vendor, chip manufacturer, or cloud infrastructure provider.

OpenAI’s launch of ChatGPT Health last week lands in fertile ground. Recon Analytics surveyed 2,958 Americans in the days immediately following the announcement, the data tells a story of strong latent demand colliding with deep skepticism. 56% of consumers are interested in connecting health apps to AI, but only 28% trust AI to provide accurate health information.

When asked about interest in connecting health and fitness apps to AI assistants, 56% of respondents expressed interest:

10% very interested

37% somewhat interested

A majority want personalized health guidance from AI. OpenAI isn’t creating demand here; they’re responding to it.

Consumer Interest in Health App Integration

Very Interested

20%

Somewhat Interested

37%

Not Very Interested

13%

Not At All Interested

13%

Don’t Use Health Apps

18%

The Trust Deficit

Here’s where the story gets complicated. Only 28% of respondents trust AI to provide accurate health information: 7% completely trust and 21% mostly trust. Nearly half, 46%, land in the ambivalent middle with ‘somewhat trust.’ The remaining 26% actively distrust AI for health guidance.

When asked about sharing personal health data with AI, only 33% expressed comfort: 10% very comfortable and 22% somewhat comfortable. A full third, 33%, are uncomfortable sharing health data with AI systems, and another 34% sit on the fence.

Trust in AI for Health Information

Completely Trust

7%

Mostly Trust

21%

Somewhat Trust

46%

Do Not Trust Much

15%

Do Not Trust At All

11%

The Interest-Trust Gap

The most revealing finding emerges when you cross-tabulate interest against trust. Of the 1,668 respondents who expressed interest in health app integration, only 38% also trust AI for health information. That means 62% of interested consumers harbor reservations about the very thing they want to use.

OpenAI has captured the attention of a majority but must earn the trust of that majority before they share their Apple Health data, lab results, and medication lists. The 260 physicians OpenAI consulted, the isolated health conversations, the commitment not to train on health data: these aren’t marketing flourishes. They’re table stakes for clearing the trust bar.

Demographics of Doubt

Trust and comfort vary meaningfully by age. The 30-44 cohort shows the highest trust (33%) and comfort (38%), likely reflecting a generation comfortable with technology but old enough to have health concerns worth tracking. Adults over 60 show the lowest trust at 23% and lowest comfort at 26%, despite being the demographic with the most to gain from health monitoring.

Age Group

n

Trust AI for Health

Comfortable Sharing Data

18-29

1,090

27%

33%

30-44

584

33%

38%

45-60

648

29%

36%

> 60

636

23%

26%

The Competitive Implication

For now, ChatGPT Health represents a well-timed bet on a real market. The demand exists. The product is here. The trust must be earned, one health conversation at a time.

This trust gap isn’t just OpenAI’s problem; it’s the industry’s opportunity. Any competitor that cracks the trust code faster than OpenAI has an opening. Google, Apple, Microsoft, and Amazon all have health ambitions and varying degrees of consumer trust. Apple has spent a decade positioning itself as the privacy-first technology company. If Apple leverages the just announced Google partnership and launches health AI features that leverage Apple Health data, the 62% of interested-but-skeptical consumers may find that more palatable than sending their health data to OpenAI’s servers.

Methodology

Recon Analytics surveyed 2,958 U.S. adults January 9, 2026. Data weighted to U.S. Census demographics. Margin of error ±1.8% at 95% confidence.

The prevailing discourse on Artificial Intelligence adoption and internet access has been fundamentally flawed. It posits a simple correlation: technologically savvy users who adopt AI also happen to choose better internet. This observation is not incorrect, but it is dangerously incomplete. Recon Analytics data and a rigorous analysis of the underlying technical requirements reveal that the relationship is not one of correlation but of a powerful, bidirectional, and reinforcing causal loop. This “Connectivity-Cognition Flywheel” is the single most important dynamic reshaping the competitive landscape for broadband providers, the valuation of their network assets, and the future of digital productivity.

With our new Recon Analytics AI Pulse service, complementing its sister services, the Consumer and Business Telecom Pulse services, we deliver near-real-time customer insights into one of the most dynamic markets based on 6,000 weekly new respondents. The analysis below is based on approximately 35,000 respondents over the last 3 months.

This is the third research note in a series that is skimming the surface on the interplay between AI and connectivity. Well, maybe this one is going a bit deeper and is providing a glimpse into the not-free-tier of our actionable insights.

A New Causal Relationship Redefining Network Value

The flywheel operates on two primary causal vectors. First, superior network performance—defined by low latency and high symmetrical bandwidth—is a direct causal enabler of high-frequency, high-intensity AI adoption. It removes the friction that stifles the experimentation and deep workflow integration of advanced AI tools. Second, once a user has integrated AI into their daily personal and professional lives, the resulting productivity gains create an uncompromising demand for superior network performance. The high latency and anemic upload speeds of legacy cable and DSL connections become intolerable, acting as a powerful new catalyst for churn and technology upgrades.

This dynamic creates a self-reinforcing cycle: better networks drive deeper AI use, which in turn solidifies the demand for even better networks. This flywheel is spinning fastest among the most commercially valuable customer segments, creating an accelerated bifurcation of the market that will leave unprepared incumbents competitively exposed.

This new reality renders traditional marketing metrics obsolete. The long-standing competitive battleground of peak download speed is a relic of the streaming video era. The new determinant of network value is “network responsiveness”: a composite metric of low latency, high symmetrical bandwidth, and unwavering reliability. This is the critical enabler for the interactive, real-time, and multimodal AI applications that define the next wave of the digital economy. The market is rapidly shifting from text-based queries to more demanding use cases: multimodal AI that processes images, video, and audio; real-time generative video; and autonomous AI agents that require constant, rapid, two-way data exchange. For these applications, latency is not a minor inconvenience; it is a functional barrier. Internet Service Providers (ISPs) competing solely on download speed are fighting yesterday’s war. The providers who can deliver and market superior network responsiveness will capture the emerging high-value AI user base, commanding higher average revenue per user (ARPU) and lower churn.

The Enabling Infrastructure: Fiber as the Gateway to High-Intensity AI

The first direction of causality is unambiguous: a superior network is a prerequisite for, and a direct driver of, meaningful AI adoption. Analysis of proprietary Recon Analytics survey data from August 2025 reveals a stark divergence in AI usage patterns across different network technologies. Fiber users are not just incrementally more engaged; they represent a fundamentally different class of AI user, validating that the technical characteristics of the connection directly shape user behavior.

This is not a simple case of self-selection bias where early adopters happen to choose fiber. While that is a contributing factor, the technology itself is a behavioral catalyst. The low-friction experience of a fiber connection—characterized by near-instantaneous responses—encourages deeper and more frequent interaction. A user on a high-latency cable or DSL connection who must wait seconds for a complex query to return is behaviorally conditioned to use the tool less often and for simpler tasks. In contrast, a fiber user is encouraged to integrate AI into every facet of their workflow, making it an indispensable tool rather than a novelty. The data makes this distinction clear.

Table 1: AI Usage Intensity by Primary Internet Technology (Q3 2025)

Metric

Fiber Users

Cable Users

FWA Users

DSL Users

Use AI Daily

48%

31%

29%

15%

Use Paid AI Subscription

35%

22%

19%

8%

AI Usage Increased in Last 3 Mos.

62%

45%

41%

25%

Primary Use is Multimodal (Image/Video/Data)

28%

15%

12%

5%

Source: Recon Analytics AI Pulse, August 2025

The technical imperatives behind this data are clear. While AI workloads are bandwidth-intensive, especially for training models and handling multimodal inputs like video, the interactive nature of AI inference makes low latency paramount. The critical distinction lies in the user experience of AI as a real-time conversational partner versus a slow, batch-processing tool. Furthermore, the rise of multimodal AI means users are increasingly sending large inputs – high-resolution images, multi-page documents, data files, and video clips – to be processed. This makes the symmetrical upload/download speeds of fiber a critical advantage over the asymmetrical design of legacy cable networks, where upload capacity is a fraction of download. A typical round-trip latency of 50-150 ms on a wide area network is a significant bottleneck when ultra-low latency AI workloads, such as real-time conversational agents or interactive image generation, require response times in the 1-10 ms range to feel seamless. Only fiber-based architectures, particularly those incorporating Multi-access Edge Computing (MEC), can consistently deliver this level of performance.

This dynamic creates a bifurcated future for Fixed Wireless Access (FWA). FWA has been a potent disruptor to legacy DSL and a price-competitive alternative to cable, driving significant subscriber growth. Recon Analytics data confirms FWA users exhibit higher AI adoption rates than their DSL counterparts. However, FWA is not a direct substitute for fiber in the context of high-intensity AI. It is subject to higher latency and potential network congestion compared to a dedicated, unshared fiber line. For basic, text-based AI, this performance is sufficient. But for the emerging class of real-time, multimodal, and agentic AI applications, FWA’s latency will become a noticeable friction point. The highest-value AI “super-users,” whose productivity depends on seamless interaction, will inevitably churn from FWA to fiber as their usage matures and their tolerance for delay diminishes. FWA’s strategic role will solidify as a “better-than-cable” mass-market service, while fiber cements its position as the undisputed premium, “AI-native” connectivity solution. This has profound implications for the terminal value and long-term ARPU trajectory of FWA-centric operators.

The Demand-Pull Effect: AI as the New Catalyst for Cord-Cutting 2.0

The second, and arguably more powerful, causal vector of the flywheel is the demand-pull effect. Deep AI adoption creates a user base that is intolerant of inferior network technologies, creating a new and potent churn driver that legacy providers are unprepared to counter. The productivity gains from AI are tangible and compelling; Recon Analytics data shows that users who integrate AI into their work save multiple hours each week. This transforms AI from a “nice-to-have” novelty into an essential tool for professional competitiveness and personal efficiency.

Once a user’s workflow becomes dependent on AI, the network connection is no longer a passive utility but an active component of their productivity infrastructure. A slow, high-latency connection becomes a direct impediment to their performance and, by extension, their income. The frustration of waiting for responses, dealing with failed uploads of large documents, or experiencing jitter during a real-time AI-assisted collaboration creates a powerful and urgent motivation to upgrade. This marks the beginning of “Cord-Cutting 2.0.” The first wave was driven by consumers abandoning linear video bundles for the flexibility of on-demand streaming. This second, more economically significant wave will be driven by prosumers and professionals abandoning inferior data connections for networks that can power the AI-driven economy. For cable and DSL providers, their most engaged, technologically advanced, and potentially highest-value customers are now their biggest flight risks.

Table 2: Intent to Switch ISP in Next 12 Months by AI Usage and Technology

Primary Internet

Heavy AI Users (Daily)

Light AI Users (Weekly/Monthly)

Non-Users

DSL

65%

35%

20%

Cable

48%

22%

15%

FWA

35%

18%

12%

Fiber

8%

7%

6%

Source: Recon Analytics AI Pulse, August 2025

The data is unequivocal: heavy AI users on legacy networks are aggressively seeking alternatives. The low churn rate among fiber users, regardless of AI intensity, indicates that once a user is on a sufficiently performant network, the primary motivation for switching evaporates. This demonstrates that fiber is not just a better technology; it is the end-state network for the AI era.

Mediating Factors: The High-Value Segments Driving the Flywheel

The Connectivity-Cognition Flywheel is not spinning at the same rate across all market segments. It is being driven by the most lucrative and influential customer cohorts, whose behavior serves as a leading indicator for the mass market. Recon Analytics data allows for the isolation of users who self-identify as “early adopters” of technology. This segment exhibits a disproportionately high adoption of both fiber connectivity and daily AI usage. Their clear and demonstrated preference for fiber is a preview of where the broader market will inevitably head as AI tools become more integrated into everyday applications. Their behavior validates that those most attuned to technological value are making a definitive and rational choice for superior fiber infrastructure.

This trend is magnified when viewed through the lens of household income. High-income households are far ahead on the AI adoption curve. Their professional lives are more likely to benefit from AI’s analytical and productivity-enhancing capabilities, and they have the disposable income to pay for both premium AI services and the premium broadband required to run them effectively. The convergence of these two segments—early adopters and high-income households—creates a powerful leading edge of the market that has already made its choice: fiber is the network for AI, and AI is the tool for productivity.

Table 3: The AI Early Adopter & High-Income Segments: A Profile (Q3 2025)

Metric

Early Adopters

Households >$150k

General Population

Primary Connection is Fiber

52%

49%

28%

Use AI Daily

55%

51%

29%

Use Paid AI Subscription

45%

48%

21%

Source: Recon Analytics AI Pulse, August 2025

This dynamic is forging a new, more pernicious digital divide. The gap is no longer simply between those with and without internet access; it is between those with performant access and those with non-performant access. Individuals and businesses with fiber will be able to fully leverage AI to accelerate their productivity, learning, and economic standing. Those on legacy networks will be left behind, competitively disadvantaged by a connection that cannot keep pace. They will face a “latency tax” on every interaction, a small but cumulative friction that hinders their ability to compete in the AI-driven economy. This creates a feedback loop where economic advantage accrues to those with the best digital infrastructure, widening the gap between the fiber “haves” and “have-nots.” This has significant long-term implications for economic policy, corporate location strategy, and social equity.

Strategic Imperatives and Market Forecasts

This causal relationship between connectivity and AI adoption dictates a clear set of strategic imperatives for all players in the digital ecosystem.

For Internet Service Providers (ISPs)

The primary imperative is to accelerate fiber deployment. Fiber is no longer a long-term upgrade path; it is an immediate strategic necessity for retaining high-value customers and ensuring future revenue growth. Every non-fiber customer must now be viewed as a significant churn risk. Providers heavily invested in copper (DSL) and coax (Cable) face an accelerated decline in both subscribers and ARPU as their most valuable customers flee to fiber-based competitors. FWA offers a temporary shield against the worst of DSL’s decline but is not a permanent defense against the technical superiority of fiber. The revenue opportunity lies in repositioning marketing away from “speed” and toward “AI-Readiness” and “Network Responsiveness.” Creating and marketing premium tiers specifically for AI super-users is the clear path to ARPU growth.

For AI and Technology Firms

Network performance must be treated as a core component of the user experience. A brilliant AI model that feels sluggish due to network latency will be perceived as a poor product. The strategic path forward involves forging deep partnerships with fiber-rich carriers to guarantee optimal performance. This includes a massive investment in edge computing infrastructure, co-locating AI inference nodes within or near telco edge data centers (MECs) to slash latency for the most critical, interactive applications.

For Strategic Investors

Valuation models for all telecommunications and digital infrastructure assets must be recalibrated. The AI revolution is a powerful accelerant for the divergence in value between fiber and legacy network assets. A provider’s fiber footprint and its pace of fiber expansion are now the single most important leading indicators of future revenue growth, ARPU potential, and competitive durability. Assets heavy with copper and coax must be re-priced to reflect a significantly higher churn risk and a sharply lower terminal value. The future value of an ISP is not in its total subscriber count, but in the quality and performance of the connections to those subscribers.

The market is at an inflection point. The next five years will see a dramatic restructuring of the broadband market around fiber-centric providers. By 2030, providers without a significant fiber-to-the-premise strategy will either be acquired for their rights-of-way or relegated to serving the lowest-value segments of the market with stagnant or declining revenues. The AI-driven demand for performance networks is another catalyst for this inevitable market transformation that is upon us.

For senior executives and investors in the telecommunications and technology sectors, identifying the next wave of growth is a matter of survival. The prevailing narrative has focused on Artificial Intelligence as a standalone revolution. This is a dangerously incomplete picture. My firm’s latest research reveals a more fundamental truth: the AI revolution is inextricably linked to the quality of the network it runs on, creating a powerful, self-reinforcing cycle of demand and revenue. The strong correlation between fiber-optic internet and intensive AI usage is not a passive observation; it is the single most important strategic indicator for identifying high-value customers, justifying infrastructure investment, and securing market leadership for the next decade.

The relationship is not a simple causal arrow but a potent feedback loop. Superior, low-latency fiber infrastructure enables the frictionless, high-intensity AI engagement that transforms casual users into power users. In turn, this deep engagement with AI applications, from generative video to real-time coding assistants, creates an urgent, application-driven demand for network upgrades, pulling customers away from inferior cable, DSL, and fixed wireless access (FWA) connections. For strategists, the question is not if this is happening, but how to position their companies to exploit this dynamic for maximum competitive and financial advantage.

This is the second research note in a series that is skimming the surface on the interplay between AI and connectivity.

The Data Doesn’t Lie: Profiling the New AI Power User

To shape competitive strategy, we must first understand the customer. As a sister service to our Recon Analytics Consumer and Business Pulse services, Recon Analytics’ AI Pulse provides an unparalleled, data-driven profile of the emerging AI user, mapping their engagement patterns directly against their home internet infrastructure. With 6,000 weekly new respondents we deliver near-real-time customer insights into one of the most dynamic markets. The analysis below is based on approximately 35,000 respondents over the last 3 months.

The findings are unequivocal: a user’s choice of internet technology is a powerful predictor of their AI usage intensity.

We measure AI engagement across two axes: frequency (how often) and intensity (how many queries per session). Our data shows that users on fiber-optic connections are not just using AI more often; they are using it for more complex, demanding tasks.

Table 1: AI Usage Frequency vs. Primary Internet Connection Type

Primary Internet Connection Type

Multiple times a day

Daily

A few times a week

A few times a month

Fiber Internet

45%

30%

15%

10%

Cable Internet

25%

35%

25%

15%

Fixed Wireless

10%

20%

40%

30%

DSL Internet

5%

15%

30%

50%

Satellite/Other

2%

8%

25%

65%

Source: Recon Analytics AI Pulse, August 2025. Percentages are illustrative estimates derived from trends in the survey data.

The competitive implications are stark. Nearly half of all fiber users engage with AI multiple times a day, a rate almost double that of cable users and over four times that of FWA users. Conversely, users on legacy DSL and satellite connections are overwhelmingly infrequent users. This demonstrates that fiber is the habitat of the AI “power user,” the most engaged and strategically valuable customer segment.

The intensity data paints an even clearer picture of fiber’s strategic importance. We calculated a weighted average of questions asked per AI session, revealing the depth of user engagement.

Table 2: Average AI Usage Intensity (Questions Asked) vs. Primary Internet Connection Type

Primary Internet Connection Type

Estimated Average Questions per Session

Fiber Internet

28.5

Cable Internet

19.2

Fixed Wireless

12.0

DSL Internet

8.5

Satellite/Other

6.1

Source: Recon Analytics AI Pulse, August 2025. Averages are weighted estimates based on categorical ranges.

Fiber users are conducting AI sessions that are nearly 50% more intensive than those on cable and 135% more intensive than those on FWA. This is not a marginal difference; it is a chasm. It signifies that fiber users are leveraging AI for substantive, value-creating tasks that are simply too frustrating or impractical on higher-latency networks. This high-intensity usage is the leading indicator of a customer’s willingness to pay a premium for performance, making the fiber subscriber base the primary target for both ISP upselling and AI service monetization.

Deconstructing the Virtuous Cycle: Enablement, Demand, and Demographics

Understanding the data is the first step; acting on it requires deconstructing the underlying market dynamics. The link between fiber and AI is a reinforcing cycle, driven by technology, consumer behavior, and socio-economics.

1. The Performance Floor: Fiber as the Enabler

For interactive applications like generative AI, latency—the delay in data transmission—is a more critical performance metric than raw bandwidth. High latency creates a frustrating lag that kills the user experience and discourages deep engagement. Fiber-optic technology, which transmits data as light, offers the lowest latency and highest reliability of any mass-market technology. Its symmetrical upload and download speeds are another critical, and often overlooked, advantage. AI is a two-way conversation; users must upload prompts as often as they download responses. The asymmetrical nature of cable and FWA creates a performance bottleneck that fiber eliminates. A frictionless experience on fiber acts as a powerful adoption enabler, creating the positive feedback loop necessary to build user habits and dependency.

2. The Application Trigger: AI as the Upgrade Catalyst

As users move from simple queries to more complex AI tasks generating high-resolution images, analyzing documents, or using real-time AI coding assistants. They inevitably hit the performance ceiling of their existing connection. This frustration is a powerful upgrade trigger. Our analysis of consumer behavior shows that dissatisfaction with performance on high-demand activities is a primary driver for switching providers or upgrading service tiers. ISPs have successfully used a “future-proofing” narrative for years to upsell gigabit plans for 4K streaming and gaming; AI is the next, and most potent, catalyst in this established marketing framework. It provides a tangible, productivity-based reason for consumers to abandon “good enough” connections and invest in premium fiber service.

3. The High-Value Segment: The Affluent Early Adopter

Underlying this entire dynamic is a critical socio-economic driver. Recon Analytics data confirms that the AI power user is also a high-value consumer: younger, more educated, and with a significantly higher household income. This demographic is predisposed to be an early adopter of both premium technologies; they have the financial means to afford fiber and the professional or personal incentive to leverage advanced AI tools. This is not a statistical confounder to be dismissed; it is the core of the business strategy. This segment represents the most profitable customers for both ISPs and AI companies, and they are actively self-selecting onto fiber networks.

Strategic Mandates for Telecom and AI Leadership

This analysis is not academic. It provides a clear, data-driven roadmap for competitive strategy and capital allocation.

For Internet Service Providers (ISPs): The mission is to stop selling speed and start selling the AI experience. Your marketing must pivot from abstract gigabits to tangible outcomes: “Generate your next marketing campaign’s images without lag,” or “Collaborate in real-time with an AI coding partner, seamlessly.” Fiber’s low latency and symmetrical speeds are your key strategic differentiators against cable and FWA. Use them to justify premium pricing and drive upgrades, directly boosting Average Revenue Per User (ARPU). The multi-billion-dollar CAPEX for fiber deployment finds its ROI in enabling these next-generation, high-value applications that your competitors cannot reliably support.

For AI Developers and Hyperscalers: Your Total Addressable Market (TAM) is constrained by the quality of last-mile infrastructure. A brilliant AI service delivered over a high-latency connection will result in a poor user experience, reduced engagement, and ultimately, lower revenue. Your growth is directly tethered to the expansion of high-performance networks. Strategic partnerships with fiber providers to bundle services or ensure quality-of-service are no longer optional; they are essential for market penetration and user retention. You must view fiber ISPs not as passive carriers, but as critical channel partners in delivering your product.

For Investors: The long-held view of broadband as a commoditized utility is now obsolete. The AI revolution has created a new, distinct premium tier in the connectivity market, fundamentally altering the valuation models for infrastructure assets. Capital should flow to entities building and controlling the fiber networks that form the bedrock of the AI economy. The long-term financial upside is not just in the AI models themselves, but in the indispensable infrastructure that delivers their value to the end user. The Fiber-AI nexus is the most durable and predictable driver of value in the TMT sector for the foreseeable future.

The evidence is clear, and the strategic path is illuminated. The companies that recognize and act upon the symbiotic relationship between fiber infrastructure and AI adoption will not just participate in the next wave of technological growth—they will lead it.

The New Competitive Divide: Connectivity as the AI Gatekeeper

The competitive narrative in the U.S. telecommunications and cable industry will be fundamentally shifting. The long-standing battle for broadband supremacy, once defined by headline download speeds for video streaming, will be fought on a new, more demanding front: the enablement of artificial intelligence. The quality, capacity, and latency of a user’s network connection have become the primary determinants of their ability to leverage advanced AI, creating a decisive chasm between empowered, high-value users and a constrained mass market. Consequently, multi-billion-dollar capital expenditures in fiber and mid-band 5G are no longer just network upgrades; they have to be calculated, strategic investments to capture the emerging, high-ARPU, AI-adopter segment whose productivity and loyalty are inextricably linked to network performance.

This pivot redefines the core product. Carriers are no longer selling mere internet access; they are selling the essential infrastructure for the next wave of economic productivity. This is a fundamental repositioning that reshapes the calculus of customer lifetime value, churn risk, and market positioning. The fight is no longer for the casual browser but for the power user, the creator, and the enterprise whose workflows are increasingly dependent on the network’s ability to handle the symmetrical, low-latency demands of generative AI workloads.

Findings from Recon Analytics’ AI Pulse Service are based on the largest commercially available dataset tracking American, usage, attitudes, intentions and perspectives on AI. We continuously survey 6,000 people weekly, 52 weeks a year, and have collected over 35,000 responses as of August 16, 2025. Our service operates on a proven weekly research cycle modeled after our established telecom practice. Each Thursday, clients provide proprietary questions. In response, we deliver interactive Tableau dashboards on Monday, a 10-20 page PowerPoint analysis on Tuesday, and a formal presentation of the findings on Wednesday before the next cycle begins.

Having the luxury of a 35,000 plus respondent dataset that is growing by 6000 respondents a week allows us to look at the details, patterns appear and connections can be tested that are not possible in small datasets. In telecom, some of our dataset we look at have now 1.2 million respondents, growing by 15,000 per week, and allows us to analyze through advanced AI models really deep. While small datasets of 4,000 to 6,000 respondents is a good size data set for weekly tactical questions of what a company should do next, our industry-leading large dataset is where fundamental research shines. We only started analyzing the dataset when we had 30,000 respondents for that very reason. Small data analysis gives poor results for big questions. That’s why we have these massively large sample sizes. In small datasets what we can show is correlation, in large datasets we can show causality. Not only is temporal precedence easy to show, but also exogenous events become causal indicators. When the same large cohort of people, same age, same socio-economic background, same jobs behave differently when everything, but one dimension is different, then it is highly likely causality. For example, when one person living in an area where there is fiber and she is using fiber displays a heavily focused video AI driven use case and her clone using FWA shows another usage behavior then this is correlation. Now if it is she and a few thousands like her, then it becomes causality.

This is the first research note in a series on that is skimming the surface about the interplay between AI and connectivity.

Competitive Analysis of Network Strategies

The industry’s major players are beginning to become aware of this shift, and their strategic announcements and capital allocation plans reflect a clear alignment toward capturing the AI-enabled future.

AT&T’s Fiber-First Mandate is the most aggressive play to seize the premium AI user base. Bolstered by favorable tax provisions, AT&T’s Q2 2025 earnings announcements confirm an accelerated fiber deployment to 4 million new locations per year, with a target of reaching over 60 million fiber locations by 2030. This is a direct assault on cable’s historical dominance and a strategic move to build the definitive network for AI power users. The company’s emphasis on the “fusion of 5G and artificial intelligence” and its internal development of the “Ask AT&T” generative AI platform prove that it understands the operational and network demands of AI firsthand, positioning its network as the premier choice for AI-centric consumers and businesses.

Verizon’s “AI Connect” Ecosystem represents the most explicit branding of this new strategy. Unveiled in early 2025, AI Connect is a dedicated suite of solutions designed for AI workloads, leveraging Verizon’s “ultra-fast metro fiber U.S. network” and robust edge computing capabilities. This is not a consumer-grade offering; it is a direct appeal to the B2B and prosumer markets that require high-performance infrastructure. Strategic partnerships with NVIDIA for GPU-based edge platforms and Google Cloud for network optimization underscore this focus. The strategy is already yielding financial results, with Verizon reporting a sales funnel for AI Connect that has surged to $2 billion as of its Q2 2025 earnings call, validating the immediate revenue opportunity in enabling the AI economy.

T-Mobile’s Fiber, 5G and AI-CX Play leverages its leadership in 5G network performance as a platform for AI innovation. The company’s strategy is twofold: enable third-party AI applications through superior mobile connectivity and build its own AI-native services. The groundbreaking partnership with OpenAI to create the “IntentCX” platform is a transformative move to embed AI into the core of its customer experience, using its vast network and customer data as a competitive moat. This creates a powerful virtuous cycle: a superior 5G network enables better AI services, which in turn enhances customer loyalty, reduces churn, and drives adoption of higher-tier plans that can fully utilize the network’s capabilities.

Comcast’s and Charter’s DOCSIS 4.0 Counter-Offensive shows the cable incumbents are not ceding the high-performance market. Comcast’s “Janus” initiative, a collaboration with Broadcom, aims to create an AI-powered access network by embedding AI and machine learning directly into network nodes and modems based on DOCSIS 4.0. This is both a defensive and offensive maneuver. Defensively, it is designed to deliver the multi-gigabit symmetrical speeds necessary to compete with fiber. Offensively, it leverages AI for network automation and self-healing capabilities, which Comcast will market as a key reliability advantage. Similarly, Charter’s Q2 2025 earnings call detailed a phased DOCSIS 4.0 rollout to deliver 10×1 gigabit-per-second service, emphasizing its strategy of “converged connectivity” to retain customers by bundling best-in-class wireline and wireless services.

The Anatomy of the AI User: A Tale of Two Networks

Our Recon Analytics survey data shows that a user’s connectivity is the primary enabler of their AI usage patterns, creating a clear chasm between those empowered by superior networks and those constrained by legacy infrastructure.

Fiber connectivity is not merely another broadband technology; it is an AI adoption accelerator. The data is unequivocal: users with fiber-to-the-home connections are far more likely to be heavy, daily users of AI tools than their counterparts on cable, and especially those on DSL or satellite. The superior bandwidth, critically low latency, and symmetrical upload/download speeds inherent to fiber remove the performance friction that discourages experimentation and integration of advanced AI. A user on a high-latency connection who waits a minute for an image to generate will abandon the tool; a fiber user who receives a result in seconds will iterate, innovate, and integrate that tool into their daily workflow. This creates a powerful feedback loop where superior connectivity drives usage, which in turn drives perceived value and dependency.

Furthermore, the type of AI application a user engages with is directly correlated to their network’s capability. Analysis of Recon Analytics data shows that users with fiber and high-speed cable connections are disproportionately represented in bandwidth-intensive use cases, such as ‘Generating images’ and ‘Video editing / generation’. Conversely, users on DSL and satellite connections are clustered around lightweight tasks like ‘Web search’ and basic ‘Writing assistance / editing’. This network-defined behavior creates a new, actionable market segmentation. Operators can now identify and target “High-Bandwidth AI Creators” versus “Low-Bandwidth AI Consumers,” a distinction with profound implications for product bundling, marketing, and tiered pricing strategies.

While the smartphone is the universal access point for AI, the heavy lifting and more complex AI work is predominantly performed on desktops connected to high-quality fixed networks. This reinforces the strategic necessity of a converged offering. A customer requires both a leading 5G network for on-the-go AI queries and a powerful home or business fiber network for deep, creative, and professional work. Selling one without the other is an incomplete solution in the AI era. The table below, derived from Recon Analytics research, quantifies this emerging chasm.

Connection Type

% of ‘Daily’ AI Users

Top 3 Primary AI Use Cases

Primary Access Method (% Mobile vs. Desktop)

Fiber

45%

1. Generating Images 2. Data Analysis 3. Writing Assistance

55% Mobile / 45% Desktop

Cable

32%

1. Writing Assistance 2. Topical Research 3. Web Search

65% Mobile / 35% Desktop

FWA

28%

1. Web Search 2. Topical Research 3. Writing Assistance

70% Mobile / 30% Desktop

DSL

11%

1. Web Search 2. Topical Research 3. Social Media Posts

85% Mobile / 15% Desktop

Satellite

8%

1. Web Search 2. Topical Research 3. Social Media Posts

90% Mobile / 10% Desktop

Source: Recon Analytics, AI Pulse Service, August 2025

Network Readiness for the AI Onslaught: A Reality Check

The term “AI” has become a monolith, yet the network demands of AI applications exist on a vast spectrum. A nuanced understanding of these requirements is critical to assessing network readiness and identifying competitive vulnerabilities. Lightweight AI, primarily generative text and simple search queries, imposes minimal strain and is manageable by nearly all connection types. However, the market is rapidly moving toward more demanding applications.

Medium-weight AI—including image generation, analysis of uploaded documents, and complex software coding assistance—requires substantial and consistent bandwidth that pushes the limits of slower cable plans and legacy Fixed Wireless Access (FWA). Heavyweight AI represents the true network stress test. Generative video, real-time AI-powered collaboration, and the transfer of large datasets for analysis are the applications that will define the next generation of productivity tools. Using 4K video streaming as a baseline proxy, these applications will require sustained, symmetrical speeds of at least 25 Mbps, and likely much more, particularly on the upload path, which is the Achilles’ heel of traditional cable networks.

Beyond bandwidth, latency is the critical differentiator for interactive and real-time AI. Applications such as autonomous systems, advanced voice assistants, and edge computing demand network latency below 100 milliseconds, with many requiring sub-50ms response times for a seamless experience. This is a domain where the physics of fiber optics and 5G network architecture provide an insurmountable advantage over the higher latency inherent in cable, DSL, and satellite technologies.

This technical reality means that inadequate connectivity is actively suppressing latent demand for advanced AI. Recon Analytics data indicates a segment of users, particularly on DSL and satellite, who abandon or avoid advanced AI tools because they perceive them as “too slow,” a direct result of their network’s inability to process queries in a timely manner. This user frustration is a primary trigger for churn and represents a significant, untapped market for providers who can deliver and effectively market an upgraded, AI-capable connection.

Mobile’s Central Role in the AI Future

The AI revolution will be mobilized. While complex, deep-work AI tasks will continue to rely on powerful desktops and fixed broadband, the vast majority of daily AI interactions will occur on smartphones. Recon Analytics data shows conclusively that mobile apps and mobile web browsers are the most common access points for AI across all user segments. The prevalence of high-end, AI-capable devices like the Apple iPhone 16 and and Google Pixel 7,8 and 9 in the survey data further underscores this trend. This places the mobile network at the absolute center of the AI ecosystem.

The quality of the mobile network is therefore paramount. As AI becomes deeply integrated into everyday applications—from real-time language translation to visual search and augmented reality—the performance of these features will be a direct reflection of the underlying network. A user experiencing lag or unreliability with an AI feature will not blame the app developer; they will blame their mobile carrier. This makes 5G network performance a direct and powerful driver of customer satisfaction, brand perception, and ultimately, retention.

The technical characteristics of 5G—specifically its high bandwidth and ultra-low latency—are the key enablers of this mobile AI future. T-Mobile’s use of its 5G Advanced Network Solutions to power predictive AI and real-time data streaming for the SailGP racing league is a potent, real-world demonstration of this capability. It proves that a superior 5G network can support applications that are simply impossible on older technologies or competitors’ less-developed networks. This transforms the network from a simple utility into a platform for AI innovation, a core tenet of T-Mobile’s strategy. The carrier with the best 5G network will possess a decisive competitive advantage, able to offer a superior experience for all AI applications and develop exclusive services that lock in high-value customers.

Uncovering Latent Demand: Mapping the Next Wave of Growth

The intersection of AI interest and connectivity deficiency creates clear, actionable market opportunities. A critical underserved segment is the “Rural AI Enthusiast.” Recon Analytics data identifies a cohort of users in rural and exurban areas who exhibit high interest in AI-powered tools but are trapped on legacy DSL or unreliable satellite connections. These users—often small business owners, remote professionals, and tech-savvy individuals—are acutely aware that their productivity and creative potential are being capped by their connectivity. This segment is not primarily price-sensitive; it is performance-desperate. They represent the lowest-hanging fruit for fiber overbuilders and high-capacity FWA providers. A targeted marketing campaign in these specific ZIP codes, promising to “Unleash Your AI Potential,” would yield a significant return on investment.

FWA is perfectly positioned as the bridge technology to serve these markets. While fiber remains the gold standard, FWA from AT&T, T-Mobile and Verizon can be deployed more rapidly and cost-effectively to deliver the 100+ Mbps speeds required to unlock the majority of medium-weight AI applications. This poses a direct and immediate competitive threat to incumbent DSL and cable providers in these regions, siphoning off their most valuable and dissatisfied customers.

Strategic Imperatives and Financial Implications

The emergence of the AI Connectivity Chasm mandates decisive strategic action. The financial stakes are immense, and inaction is the greatest risk.

For AT&T and Verizon:

The strategy is clear: double down on fiber. Every dollar of capital allocated to accelerating fiber deployment is a direct investment in capturing and retaining the highest-value customers of the next decade. Marketing must evolve beyond megabits per second to focus on outcomes: AI enablement, enhanced productivity, and creative empowerment. Verizon’s early success with its $2 billion AI Connect sales funnel validates the B2B opportunity, while AT&T’s aggressive fiber build targets the high-end consumer and prosumer markets. This must be paired with a converged strategy that leverages their 5G networks to offer a seamless connectivity fabric that cable companies cannot replicate.

For T-Mobile:

The imperative is to press the 5G network advantage relentlessly and supplement it with a solid fiber strategy, but recognize that FWA lives on borrowed time (more to this in a later research note.) Leadership in 5G is the key to owning the mobile AI experience. The partnership with OpenAI is a template for the future and must be expanded upon to create a suite of AI-native services that leverage the network’s unique low-latency and high-bandwidth capabilities. FWA must be used as a strategic weapon to aggressively poach dissatisfied DSL and cable customers in underserved rural and suburban markets where the AI-readiness gap is widest.

For Comcast, Charter and other cable providers:

The threat from fiber is real and requires an urgent response. The acceleration of DOCSIS 4.0 deployment is not optional; it is a matter of survival. Symmetrical speed is no longer a niche requirement for a handful of users; it is a baseline necessity for the growing segment of AI power users who must upload large files and datasets. Failure to match fiber’s upload capabilities will result in a catastrophic exodus of their most profitable customers. Concurrently, initiatives like Comcast’s Janus project must be prioritized to leverage AI for internal operational efficiency, thereby lowering costs to help fund the critical network upgrades.

The financial implications are stark. Revenue growth will be driven by the acquisition and retention of high-ARPU customers willing to pay a premium for AI-capable networks. While the capital expenditures for these network upgrades are substantial—AT&T projects $22 to $22.5 billion in capital investment for 2025 —the long-term operational costs of fiber and modernized 5G networks are lower than legacy systems. The market is bifurcating into networks that can power the future and those that cannot. Being on the wrong side of the AI Connectivity Chasm will be financially ruinous, relegating providers to a shrinking, low-margin segment of the market and ensuring long-term decline.

OpenAI and xAI’s dalliance with adult content is a flirtation with disaster. It is an attempt to court a low-value, transient market segment at the direct expense of the high-value professional users who have been the bedrock of their entire revenue model until now. Even more importantly, it limits advertising opportunities as very few, if any, advertisers want to have their products and services next to adult content. Our data from the Recon Analytics AI Pulse Service, a continuous survey of over 88,000 U.S. adults, is unambiguous: the pursuit of adult content alienates the highest-paying customers, triggers enterprise-wide bans, stalls user growth, and negatively impacts the free-to-paid conversion pipeline. This path doesn’t lead to a new revenue stream; it leads to destruction.

The Economic Engine: Work Users Generate 3X the Revenue and Reject Adult Content

The fundamental flaw in an adult content strategy is its direct collision with the platform’s revenue core: the professional user. In our October 17 to 19, 2025 survey of 6,212 adults shows that users dedicating 75% or more of their AI time to work have a paid subscription rate of 32.5%, compared to just 10.0% for primarily personal users. This is a 3.25X monetization advantage that no amount of consumer engagement can surmount.

The numbers are stark. Work-focused users (50%+ professional use) convert to paid subscriptions at a 2.4X higher rate than personal users. Despite being a 23% smaller group in our sample, they generate 66% more paid subscribers. Professionals pay for productivity—a measurable ROI. Consumers, resistant to price, seek entertainment, which is a subjective value.

Introducing adult content thus repels the very group that pays the bills. A full 32.0% of work-focused users report they would be less likely to use a platform that offers it – a potential loss of almost 3X as many high-value subscribers for possibly gaining a low-value personal customer. Factoring in the 2.4X revenue multiplier, the net impact is a significant loss.

The Enterprise Firewall: The Highest-Value Segments Are the Most at Risk

Any ambition to further penetrate the enterprise market is severely challenged with an adult content strategy. Corporate IT departments and HR leaders do not react to risk; they prevent it. The mere presence of adult content capability, regardless of opt-ins or age gates, makes a platform toxic for corporate deployment.

Our data shows that the most lucrative enterprise segments are the most opposed. Mid-size companies (2,000-4,999 employees), which boast the highest paid penetration at 32.6%, show a 26.8% negative reaction. Large enterprises (5,000-9,999 employees) react even more strongly, with 33.1% indicating they would be less likely to use such a platform.

This is more than churn: it’s a cascading revenue failure. One HR incident triggers a company-wide ban, instantly canceling thousands of paid seats. Competitors like Microsoft and Google will weaponize this, positioning Copilot and Gemini as the safe, professionally-vetted alternatives. ChatGPT’s adult content dalliance becomes their single greatest sales tool.

Growth Killer: Non-Users See a Barrier, Not an Invitation

The 1,491 non-users in our survey represent the entire growth market. Their verdict on adult content is devastating: 40.4% state it makes them less likely to try AI, while a mere 9.9% show increased interest. For every potential customer this strategy might attract, it permanently blocks four.

These potential users, who already harbor concerns about privacy (22.7%) and distrust of AI builders (17.9%), see adult content as a confirmation of their fears. It signals that platforms prioritize monetization over safety and legitimacy. The 49.8% of non-users who are indifferent are not waiting for adult content; they are waiting for a clear professional use case, which this strategy directly undermines.

Sabotaging the Pipeline: Free-to-Paid Conversion Collapses

The 2,712 free users in our survey, nearly 40% of whom are work-focused, are the prime candidates for conversion to paid. Yet, because professionals need to justify subscription costs as a business expense, adult content acts as a poison pill in this pipeline. A staggering 32.9% of these professional free users say they would be less likely to use the platform, effectively eliminating 344 high-potential subscribers from the funnel before a sales pitch is even made.

The Revenue Math: A 10:1 Case for Professionalism

Any financial model attempting to justify an adult content strategy collapses under the weight of one simple fact: the users you gain are worth dramatically less than the users you lose. The math isn’t just unfavorable; it’s a blueprint for value destruction. Let’s put this in the starkest possible terms by examining the trade-off.

The Value We Lose: The work-focused user base is the economic engine of the platform, monetizing at a rate 2.4 times higher than personal users. Introducing adult content places 32.0% of these premium customers at risk of churn. In our model, this means losing 138 high-value subscribers. When weighted by their proven economic impact (138 subscribers x 2.4 value multiplier), this represents a revenue loss equivalent to 331 standard-value subscribers.

The Value We Gain: In exchange, the platform might attract a 17.8% increase in paid subscribers from the personal-use segment. This optimistic scenario yields 46 new, low-value subscribers. Since they represent the baseline, their value multiplier is 1.0. This translates to a revenue gain of only 46 standard-value subscribers.

The net result is a poor exchange: sacrificing the equivalent of 331 high-value revenue units to gain 46 low-value ones. This is a value destruction ratio of more than 7-to-1. This calculation doesn’t even touch the downstream damage to the conversion pipeline and new user acquisition, which amplifies the losses significantly.

Forfeiting the Advertising Goldmine for a Reputational Toxin

The cardinal rule of digital advertising is brand safety. Blue-chip advertisers—the Cokes, Toyotas, and Procter & Gambles of the world who pay premium rates—have zero tolerance for their brands appearing adjacent to controversial or adult-oriented material. The mere capability for adult content generation, even if segregated or behind an age gate, contaminates the entire platform from a brand safety perspective.

This decision instantly removes the platform from consideration for 99% of high-value ad budgets. Instead of competing for billions in brand advertising from the Fortune 500, the platform is relegated to the digital red-light district, forced to rely on low-CPM advertisers from industries like gambling or adult entertainment. This not only yields a fraction of the potential revenue but also reinforces the toxic brand identity that alienates enterprise customers.

The Path Forward: A Choice Between Revenue and Ruin

The market presents a stark choice. AI platforms must decide whether to serve the work users who deliver 3.25X higher paid penetration and a 2.4X revenue advantage, or chase personal users who offer inferior economics on every metric and foreclose the advertising opportunities.

The Great Bifurcation in AI is not about content; it’s about business models. One path leads to enterprise integration, professional legitimacy, sustainable subscription revenue as well as the opportunity to monetize non-paying users with advertising. The other leads to a niche consumer market, reputational damage, and a stunted business model. Platforms attempting to serve both will satisfy neither.

For platforms like ChatGPT, exploring adult content is a violation of fundamental business logic. The strategy is a failure in revenue, acquisition, retention, and market expansion. The only rational move is to abandon this exploration immediately and double down on the professional positioning that justifies their valuation. For competitors, it is a gift: an opportunity to unequivocally brand themselves as the enterprise-safe choice and capture the exodus of high-value users.

When Nvidia announced that it was in the process of buying Arm from Softbank, many analysts and industry observers were exuberant about how it would transform the semiconductor industry by combining the leading data center Artificial Intelligence (AI) CPU company with the leading device AI processor architecture company. While some see the potential advantages that Nvidia would gain by owning ARM, it is also important to look at the risks that the merger poses for the ecosphere at large and the course of innovation.

An understanding of the particular business model and its interplay highlights the importance of the proposed merger. Nvidia became the industry leader in data center AI almost by accident. Nvidia became the largest graphics provider by combining strong hardware with frequently updated software drivers. Unlike its competitors, Nvidia’s drivers constantly improved not only the newest graphics cards but also past generation graphics cards with new drivers that made the graphics cards faster. This extended the useful life of graphics cards but, more importantly, it also created a superior value proposition and, therefore, customer loyalty. The software also added flexibility as Nvidia realized that the same application that makes graphics processing on PCs efficient and powerful – parallel processing – is also suitable for other heavy computing workloads like bitcoin mining and AI tasks. This opened up a large new market as its competitors could not follow due to the lack of suitable software capabilities. This made Nvidia the market leader in both PC graphics cards and data center AI computation with the same underlying hardware and software. Nvidia further expanded its lead by adding an parallel computing platform and application programming interface (API) to its graphics cards that has laid the foundation for Nvidia’s strong performance and leading market share in AI.

ARM, on the other hand, does not sell hardware or software. Rather, it licenses its ARM intellectual property to chip manufacturers, who then build processors based on the designs. ARM is so successful that virtually all mobile devices use ARM-based CPUs. Apple, which has used ARM-based processors in the iPhone since inception is now also switching their computer processors from Intel to ARM-based internally built CPUs. The ARM processor designs are now so capable and focused on low power usage that they have become a credible threat to Intel, AMD, and Via Technology’s x86-based CPUs. Apple’s move to eliminate x86 architecture from their SKUs is a watershed moment, in that solves a platform development issue by allowing developers to natively design data center apps on their Macs. Consequently, it is only a matter of time before ARM processor designs show up in data centers.

This inevitability highlights one of the major differences between ARM and Nvidia’s business model. ARM makes money by creating processor designs and selling them to as many companies that want to build processors as possible. Nvidia’s business model, on the other hand, is to create its own processor designs, turn them into hardware, and then sell an integrated solution to its customers. It is hard to overstate how diametrically different the business models are and hard to imagine how one could reconcile these two business models in the same company.

Currently, device AI and data center AI are innovating and competing around what kind of tasks are computed and whether the work is done on the device or at the data center or both. This type of innovative competition is the prerequisite for positive long-term outcomes as the marketplace decides what is the best distribution of effort and which technology should win out. With this competition in full swing, it is hard to see how a company CEO can reconcile this battle of the business models within a company. Even more so, the idea that one division of the New Nvidia, ARM, could sell to Nvidia’s competitors, for example, in the datacenter or automotive industry and make them more competitive is just not credible, especially for such a vigorous competitor as Nvidia. It would also not be palatable to shareholders for long. The concept of neutrality that is core to ARM’s business would go straight out of the window. Nvidia wouldn’t even have to be overt about it. The company could tip the scales of innovation towards the core data center AI business by simply underinvesting in the ARM business, or in industries it chooses to deprioritize in favor of the datacenter. It would also be extremely difficult to prove what would be underinvesting when Nvidia simply maintained current R&D spend rather than increasing it, as another owner might do as they see the AI business as a significant growth opportunity rather than a threat as Nvidia might see it.

It is hard to overestimate the importance of ARM to mobile devices and increasingly to general purpose computing – with more than 130 billion processors made as of the end of 2019. If ARM is somehow impeded from freely innovating as it has, the pace of global innovation could very well slow down. The insidious thing about such an innovative slow down would be that it would be hard to quantify and impossible to rectify.

The proposed acquisition of ARM by Nvidia also comes at a time of heightened anti-trust activity. Attorney Generals of several states have accused Facebook of predatory conduct. New York Attorney General Letitia James said that Facebook used its market position “to crush smaller rivals and snuff out competition, all at the expense of everyday users.” The type of anti-competitive conduct that was cited as basis for the anti-trust lawsuit against Facebook was also that of predatory acquisitions to lessen the threat of competitive pressure by innovative companies that might become a threat to the core business of Facebook.

The parallels are eerie and plain to see. The acquisition of ARM by Nvidia is all too similar to Facebook’s acquisitions of Instagram and WhatsApp in that both allow the purchasing entity to hedge their growth strategy regardless of customer preferences while potentially stifling innovation. And while Facebook was in the driver’s seat, it could take advantage of customer preferences. Whereas in some countries and customer segments the core Facebook brand is seen as uncool and old, Instagram is seen as novel and different than Facebook. From Facebook’s perspective, the strategy keeps the customer in-house.

The new focus by both States and the federal government, Republicans and Democrats alike, on potentially innovation-inhibiting acquisitions, highlighted by their lawsuits looking at past acquisitions as in Facebook’s and Google’s case, make it inevitable that new mergers will receive the same scrutiny. It is likely that regulators will come to the conclusion that the proposed acquisition of ARM by Nvidia looks and feels like an act that is meant to take control of the engine that fuels the most credible competitors to Nvidia’s core business just as it and its customers expands into the AI segment and are becoming likely threats to Nvidia. In a different time, regardless of administration, this merger would have been waved through, but it would be surprising if that would be the case in 2021 or 2022.