Over the past 15 years, there have been several government initiatives to expand the adoption of broadband in the United States. At the same time, industry has been busily focused on extending the reach and capacity of both fixed and mobile broadband networks. Yet, a digital divide still exists. Why? Let’s review the history here.

Since xxx, the cable and telecom industry have successfully provided broadband connectivity to more than 110.8 million households, adding about 2.4 million households per year. Gigabit speeds are now available to 85% of households. The broadband companies expand their footprint in an economically responsible way as they are accountable to their shareholders. Regardless, this leaves us with 17.7 million households left to cover. With the number of households increasing by roughly one million per year, at the current pace this would take us around 13 years. The current pandemic, with its work and study from home demands, shows us that we do not have 13 years to close this digital divide. In order to make the best possible decision on how to solve the problem, we should look at what has and has not worked in the past.

One of the most hotly debated solutions being proposed to close the digital divide is to have the government support municipal broadband, a catch-all term for providers of broadband that includes telephone and electric cooperatives. The general caveat of government entering what is a private business market is what economists call crowding out. A for-profit company typically has no chance of competing against a government entity. The latter does not have a profit goal and can provide service at a loss for an infinite period of time, as it has access to government revenue in the form of taxes or bonds to cover the losses. At the same time, the government has a poor record of innovating adjustments to a rapidly changing technological environment. The pro-municipal broadband argument holds that if for-profit companies are not offering services in a particular geographic location, they cannot be crowded out.

Electric cooperatives were founded in the 1930s to solve the 20th century equivalent of the broadband problem, and the solution is instructive for our current situation. The Institute of Local Self-Reliance, an organization in favor dispersing economic power and ownership, identified eight municipal networks that failed in the United States. The common thread of failure was inexperience in running customer-facing organizations as a neophytes struggled to learn a new skill set. This highlights the gap between running a relatively small number of government services and running much larger and more technically complicated broadband network and the problems recruiting the people with the right existing skill sets.

The most likely scenario for success is the addition of broadband service to an existing electric or telephone cooperative’s portfolio. In this case, an entity with experience in running a customer-facing operation and network for decades simply expands its service. The cooperatives are already serving mostly rural customers and do not crowd out for-profit cable and telecom providers. The FCC has recognized this and has explicitly included electric cooperatives in the Connect America Fund II initiative (which we will discuss later)

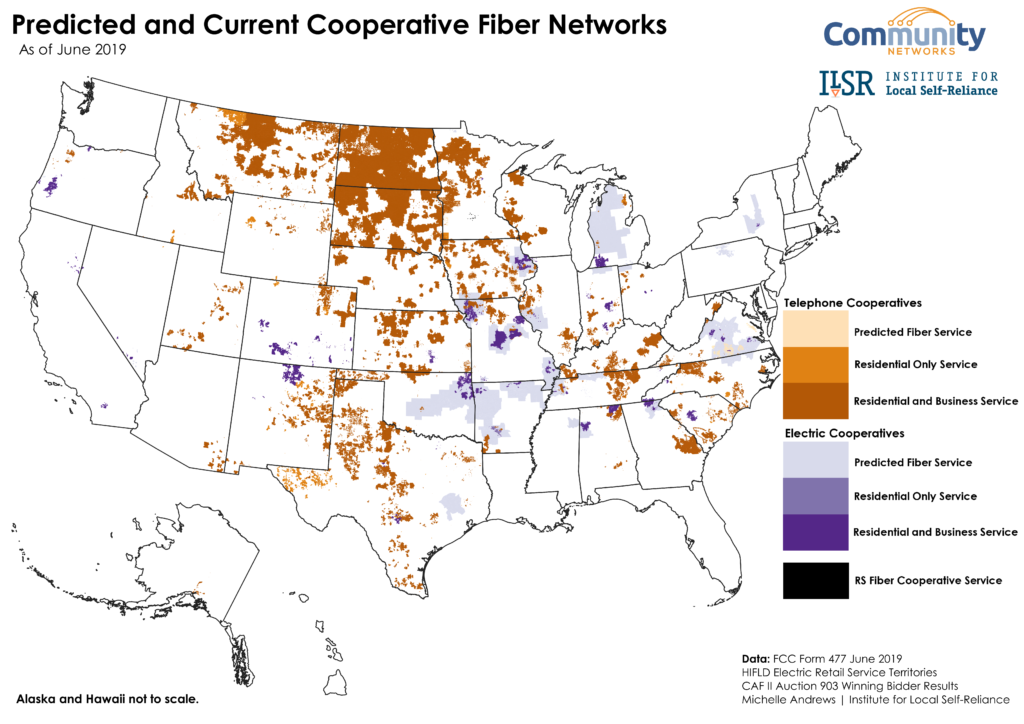

Source: ILSR

As we can see from the map above, the opportunity for rural broadband coverage from cooperatives is significant as rural areas often in the South and the Great Plains have low population density. Perhaps engaging both electric and telephone cooperatives in rural areas is an effective way to close the digital divide in some areas. These could take the form of public private partnerships and potentially avoid the pitfalls of muni-broadband.

Muni-Broadband has failed for different reasons. Research shows that most of the failed entities are urban, often engaging in direct competition with incumbent providers. Examples such as Monticello, MN, Salisbury NC, and Tacoma, WA come to mind. In other cases, the municipal broadband networks such as in Muscatine, IA, Utopia, UT had to be bailed out by taxpayers or the electric cooperative because it could not stay afloat. We also have Provo, UT and Groton, CT, which ended up selling to private companies at a great loss to tax payers, and Burlington, VT where the lack of oversight and cover-up of incompetence lead to failure to Bristol, VA where corruption meant the end of the network.

In 2010, Google announced that it would start providing broadband fiber connectivity in a number of cities to between 50,000 and 500,000 households. Cleverly, Google put out a request for information asking municipalities to apply to have Google offer fiber in their city or town. This reversed the traditional relationship between provider and municipality. Traditionally, the provider asks the municipality if it can provide service in the area. The municipality responds with what they ask for in terms of fees and extra services. Ever wondered why so many pools, parks, and sports areas are sponsored by telecom and cable companies? It was one of the demands of the city in order to allow the service provider to offer service in the town. By inverting the relationship and asking towns to apply to Google for consideration, Google shifted the power relationship, and was able to receive such favorable terms that telecom and cable providers went to cities and demanded the same terms and conditions that Google got, but they were never able to get by themselves. Under equal treatment rules, these cities had to extend the favorable Google terms and conditions to every other provider. Kansas City was the first city Google Fiber launched followed by Austin, Provo, and fifteen more cities. The Provo network was a defunct municipal network that was built for $39 million and then sold to Google for one dollar. After realizing the high cost to build a fiber network and the long delay of a payback to themselves, Google first halted further network expansions after it had deployed in five cities, and then switched to a private public partnership (PPP) model where the municipality builds the network and incurs the cost and Google sells the service. In addition, Google made an acquisition in the fixed wireless broadband space to also provide broadband wirelessly. This has slowed down the expansion significantly, but the scope has increased beyond what can be called a trial – as Google likes to call every endeavor they get into – as Google now covers 18 cities.

The 19th market for Google Fiber will be West Des Moines, Iowa. Similarly to Huntsville, Alabama, the city will build a fiber network for $39 million, in exchange Google will pay the city $2.25 for each household that connects to the network. Over the 20-year agreement, Google will pay at least $4.5 million to the city. The project will be completed by the end of 2023. By entering PPPs, Google gets the various cities to pay for the expensive built out and make money by providing the service. Google’s experience highlights that even one of the largest companies in the world does not have the focus, wherewithal and patience to actually build out a nationwide system, but relies on the government to pay for the physical buildout.

When the government helps in areas with adverse circumstances, either through low population density or low income, a business case can be made that allows the deployment of broadband services. The societal good that comes from broadband in the form of access to online learning for students, job resources for adults and an overall increase in computer skills will create greater long-term benefits than long-term costs.

On the government side of the equation, the FCC has been very focused on allocating monies (and spectrum) for broadband. The FCC’s Connect America Fund (CAF) was born out of the National Broadband Plan from 2010 aiming to broaden the availability of broadband. Now in its second iteration, CAF II, the fund is a reverse auction subsidy for broadband providers, satellite companies and electric cooperatives to provide coverage in underserved areas.

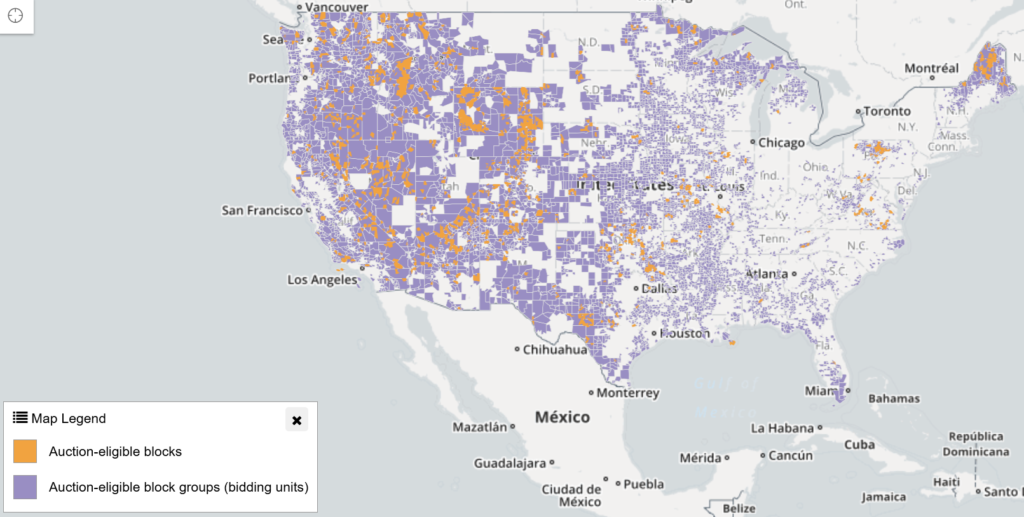

At the end of the CAF II auction, $1.49 billion of subsidies over ten years were awarded to provide broadband and voice services to 700,000 locations in 45 states highlighted in the map above. Prospective providers successively bid on who would cover the underserved market for less and less subsidy. This ensures that the area is covered for the least cost to taxpayers.

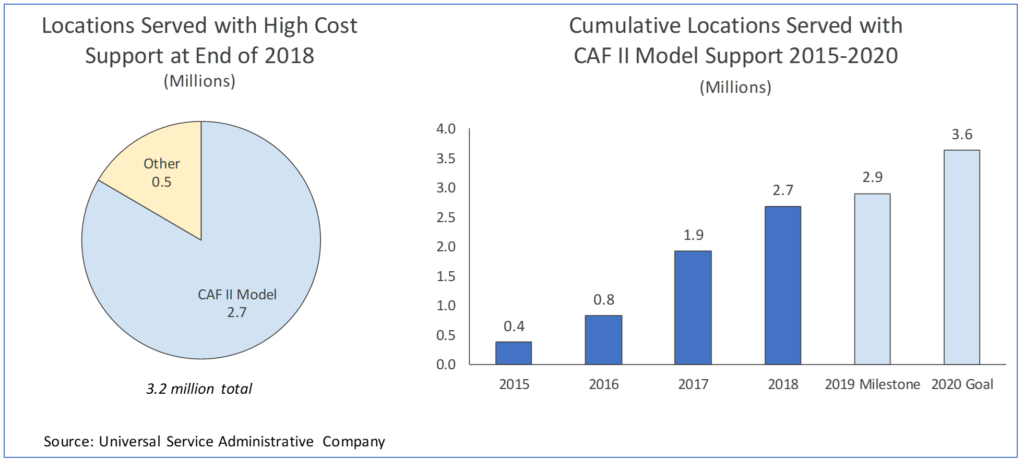

The CAF II and other government programs are increasingly closing the gap more than $20.4 billion over the next 10 years. The US Department of Agriculture has been one of the longest standing sources of support to bring broadband to rural America with $600 million per year from the ReConnect program. In October 2020, the FCC will launch the auction for the Rural Development Opportunity Fund (RDOF), a 10-year $20.4 billion program to bring broadband to areas that do not have broadband defined at 25 Mbit/ss download speed and 3 Mbit/s upload speed.

The biggest controversy around CAF II is the mapping issues. In a nutshell, if only one location in a census track has access to broadband, it is assumed that all locations have broadband. This is in a significant number of cases is not true and some locations have access when others do not. This is especially true in urban areas where we still have some high population pockets that lack access to broadband. Parts of the FCC Commission wanted to delay additional projects until the mapping problem was solved, whereas the majority voted to release the fund and work at the problem concurrently as the underserved markets are underserved even with a tighter requirement. While being criticized for its complexity and lack of clarity of how overachievement of the target goals gets recognized and impacts winning the subsidy, the program has been overall lauded a success.

When we look at what has worked and what hasn’t worked, it becomes apparent that the for-profit system has worked for 90% of Americans to have access to at least one broadband provider. The problem becomes the hard to reach, both in urban and rural environments. No matter how we look at the issue, it becomes clear that government and cooperatives plays a role to alleviate the problem as we need to fix a societal problem.

- Since Silicon Valley giants like Google with almost infinite resources have balked at building out fiber in many urban areas and are relying on cooperatives or municipalities to foot the bill, the economics of building out hard to reach parts of the United States are even more difficult.

- The broadband industry is investing between $70 billion and $80 billion per year to connect Americans, the wireless industry investing another $25 to $30 billion just shows that the industry can’t shoulder it alone.

- Electric cooperatives as non-profits have a longer time horizon, which makes their investment in underserved rural areas easier, as they have an already established customer relationship with the prospective customers and an established connection to the location.

- The CAF and other funds have worked by providing the minimal subsidy to cover underserved markets, but we just need more. Even though some have complained that it provides for only one choice ignoring that 85% of households have a choice of two wireline providers and 99% of Americans can chose between at least three mobile service providers. The counter argument for very rural parts of the United States is that one choice in an economically unprofitable market is better than no choice. Also, one has to consider that requiring every location to have two choices roughly doubles the cost of deployment and half of the infrastructure being idle.

- The program will work even better with more accurate mapping of underserved areas and through that broaden its scope from mainly rural to also urban areas and become location agnostic. If a follow-up program not only wants to bring access but also competition to an underserved area, the government would have to not only double but probably quadruple if not quintuple the subsidy due to the doubling the cost of deployment while halving the expected revenue.

The consequences of not building out areas that do not have broadband access today – regardless if urban or rural – perpetuates the current trends where we have parts of society that cannot participate in the economic and social life of our country. As 2020 has shown us, broadband internet has become the lifeline of businesses and video conferencing has become a necessity for employees to work remotely. This means that many better paid jobs are closed to people depending on where they live regardless if it is an area without broadband in the urban or rural place. Unsolved this will force a further depopulation of rural America, a flight from unserved urban areas as critical employees and business owners are effectively prevented from earning a living there. At least as important is the equal access to education. Student homework and tests cannot be counted for grading unless every student in the class is able to participate. Without broadband access, not only children who live in these unserved areas are affected but also their classmates who have access.